Brands that are forward-thinking and innovative are increasingly incorporating NFTs, or non-fungible tokens, into their marketing strategies, and they’re seeing remarkable results.

Take the example of Charmin, an American toilet paper brand, in March 2021. They posted a series of unique toilet paper-themed NFTs on Rarible, a popular marketplace for these digital assets.

Astonishingly, the highest bid for one of these unusual art pieces was more than $2000, all within the same month, demonstrating the potential value and interest in these tokens.

Fast food giant Taco Bell also ventured into the NFT space, offering its whimsical ‘Transformative Taco’ NFT collection, again on Rarible. In a spectacular demonstration of demand, the collection sold out entirely within just half an hour.

Moreover, numerous other iconic brands such as Asics, Adidas, Team GB, Coca-Cola, and Nike have also begun to explore the potential of NFTs. This shift is transforming the knowledge of how to create an NFT from a nice-to-have curiosity into a crucial skill for contemporary businesses.

How to create an NFT art

You don’t need extensive crypto knowledge. Here’s how to create NFT art:

1. Decide what you want to create and your business goal

If you don’t know where to start, you can begin by creating an NFT loyalty card or even a promotional code for your customers. You can also borrow a few NFT art ideas for inspiration.

Focus on providing real benefits to your audience. A good example is giving those who own your NFT access rights to an exclusive club or a premium service.

If you can’t make your own art, hire a freelancer to create a piece of art for you.

2. Choose a blockchain for your NFT

The most common Blockchain for NFTs is Ethereum. Other popular blockchains that hold NFTs are Binance Smart Chain, Tron, Tezos, Polkadot, EOS, Litecoin, and Cosmos.

Some factors to consider before choosing a blockchain are:

- Transaction fees on a blockchain

- The types of cryptocurrencies your audience own since they’re your target buyers

3. Sign up for a crypto wallet

Each blockchain comes with a different NFT token standard which determines which wallet will be compatible. The Ethereum NFT token standard is ETH-721, while Binance Smart Chain’s is BEP-721.

With ETH-721, you can sign up for several wallets, including Coinbase, MetaMask, and Trust Wallets. For Binance Smart Chain, you can use wallets such as MetaMask and Binance Chain Wallet.

4. Top up your crypto wallet

When you’re creating an NFT, you may have to pay transaction fees, commonly known as ‘gas’ on the Ethereum blockchain. Load your wallet with supported crypto to cover these fees.

If you are using the Coinbase wallet, you can buy crypto on Coinbase. Otherwise, purchase crypto on exchange platforms such as Binance.US, Kraken, and Gemini.

At OpenSea, one of the biggest NFT marketplaces, you’ll pay one-time registration and contract approval fees. The platform doesn’t charge you to create an NFT collection and list it for sale.

Transaction costs will depend on your NFT blockchain. Fees on the Ethereum blockchain are usually high due to the number of people making transactions. Transact during weekends or choose a less-congested blockchain like Polkadot to save on gas.

5. Choose an appropriate NFT marketplace

There are various marketplaces where you can upload your art and create an NFT: here are a few:

| Blockchain | NFT Marketplaces |

|---|---|

| Polkadot | Xeno NFT Hub |

| Tezos | Rarible, Bazaar Market, OneOf |

| Ethereum | OpenSea, Mintable, Rarible, Foundation, SuperRare, Axie Marketplace, Nifty Gateway |

-

Connect your wallet on your NFT marketplace and upload your art

Using the OpenSea marketplace as an example, here’s how to create NFT art:

-

Visit the OpenSea website and click on the ‘profile’ icon as shown below:

-

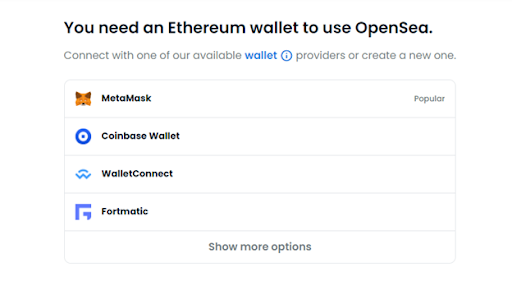

Choose your wallet and connect it

After you click on the profile icon, you’ll get a prompt to connect your wallet as shown in the image below:

Choose your wallet from the list and connect it.

-

Sign in and customize your profile

Once you’ve connected your wallet, your default name ‘unnamed’ will appear to the left of your screen with your wallet address below it as shown below:

Click ‘sign in’ on your right to update your profile by editing your username, email, image, and bio.

-

Create a new collection

Once you’ve signed in, it’s time to add your NFT to the marketplace. Click the ‘create’ button to add a new collection.

-

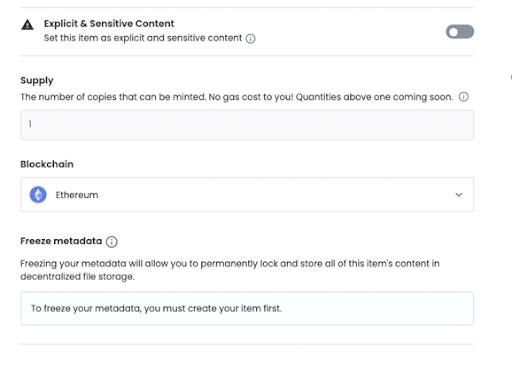

Upload a file, name it, and add a description

Once you click ‘create,’ you’ll get to a page where you can upload a file, name it, and add a description. OpenSea requires you to upload format-specific NFTs.

Source: OpenSea support

You can control various aspects of your NFT, such as the number of copies you can mint, your preferred blockchain, and whether to sell at a fixed price or go for an auction.

After you’ve customized your NFT, click ‘create,’ and your NFT will go live.

Source: OpenSea support

You’re then ready to start the process of selling your NFT!

Most Popular NFTs

While it may feel like NFTs have just exploded onto the scene, they are not a recent phenomenon. The first recorded NFT, Quantum, came into existence way back in 2014.

However, it was in 2021 when the NFT market really skyrocketed, with Quantum eventually selling for a whopping $1.4 million in June.

In terms of sheer sales numbers, the highest recorded NFT sale to date happened in December 2021. Noted artist Pak astonished the digital art world by fetching an astounding $91.8 million for ‘The Merge,’ a piece of his artwork.

Beeple, another established artist, also made significant waves in March 2021. He made the headlines after his collection of 5000 digital images earned him a jaw-dropping $69 million at a Christie’s auction.

As we moved into December 2021, NFTs like Bored Ape Yacht Club, The Sandbox, and CryptoPunks topped the popularity charts based on sales volumes, showing the diversity and breadth of interest in this exciting new asset class.

Bored Ape Yacht Club, The Sandbox, and CryptoPunks topped the list of most popular NFTs by sales volumes in the first week of December 2021.

What is an NFT and Why Spend Millions on NFTs?

NFT, standing for Non-Fungible Token, is a unique digital asset that is not exchangeable on a one-to-one basis with any other digital token.

This sets it apart from other cryptocurrencies such as Bitcoin or Ethereum, which are fungible and can be exchanged on a like-for-like basis.

NFTs are a specific kind of digital asset residing on a blockchain, the same technology underlying most cryptocurrencies.

They can be almost anything digital, including images, music tracks, audio clips, videos, or even digital collectibles.

To acquire an NFT, buyers use the specific type of cryptocurrency that is supported by the blockchain on which the NFT exists.

For example, on the Ethereum blockchain, which is one of the most popular platforms for creating and trading NFTs, buyers would use Ethereum tokens to finalize a purchase.

The motivations driving the purchase of NFTs vary widely among buyers. Some are motivated by the prestige that comes from owning original digital works created by admired artists, influencers, or globally recognized brands.

This sense of ownership and uniqueness fuels the perceived value of these tokens.

Other buyers, however, see NFTs as a form of investment. They purchase and hold on to these unique tokens in the belief that their value will increase over time, potentially leading to significant future profits.

Why should you learn how to make an NFT?

NFTs can protect your business from business losses like the infamous $31 million coupon fraud. These tokens have unique identifying codes, making them counterfeit-proof. Brands are now shifting to NFT loyalty cards and promotional and discount codes in place of traditional ones.

You can also create NFTs and use the proceeds to:

- Raise funds for charity

- Create brand awareness and increase customer engagement

- Secure funding for expansion instead of taking an expensive bank loan

Integrating NFTs with Existing Marketing Strategies

Incorporating Non-Fungible Tokens (NFTs) into existing marketing strategies presents a unique opportunity for brands to innovate and engage with their audience in a novel way. Here’s how businesses can effectively integrate NFTs into their current marketing plans:

- Enhancing Brand Storytelling: NFTs can be used to deepen brand narratives and storytelling. For instance, a brand can create NFTs that represent key moments in its history or embody its core values. This not only creates a unique connection with the audience but also adds a layer of exclusivity and prestige to the brand’s story.

- Leveraging Limited Edition Releases: Brands can release limited edition NFTs related to popular products or events, adding a digital collectible aspect to their offerings. This creates excitement and a sense of urgency among consumers, driving engagement and potentially increasing demand for both the NFTs and the associated physical products.

- Enhancing Customer Loyalty Programs: Integrate NFTs into existing loyalty programs by offering them as exclusive rewards. For example, high-value customers could be given NFTs that provide special benefits or access to unique brand experiences. This approach adds a modern twist to loyalty programs and can enhance customer retention.

- Social Media Engagement: Use NFTs to drive social media campaigns by encouraging customers to share their NFTs online. Brands can also create interactive campaigns where customers can contribute to the design of an NFT, fostering community involvement and boosting online presence.

- Charity and CSR Initiatives: Link NFT sales to charitable causes or corporate social responsibility initiatives. This not only aids in brand positioning but also appeals to socially-conscious consumers. For example, a portion of the proceeds from NFT sales could be donated to a charity, aligning brand values with social good.

- Collaborative Projects with Artists and Influencers: Collaborate with artists and influencers to create unique NFTs. This collaboration can tap into the artist’s or influencer’s existing fan base, expanding the brand’s reach and appealing to a broader audience.

- Experiential Marketing: Offer NFTs that go beyond digital art to include real-world experiences, such as exclusive access to events, behind-the-scenes tours, or meet-and-greets. This can create a more holistic and immersive brand experience.

- Cross-Promotional Ventures: Partner with other brands or platforms to create co-branded NFTs. This can help reach new audiences and add an innovative layer to cross-promotional activities.

NFTs are the future for growth-seeking small businesses

Creating NFT art can be an effective strategy to explore and unlock new growth opportunities for your business.

By tokenizing your art, you introduce a new revenue stream that can be both lucrative and sustainable.

This is because NFTs allow artists to earn royalties indefinitely each time their art is resold on the blockchain, ensuring a continuous flow of income.

Additionally, NFTs can be leveraged as a fundraising tool, enabling businesses to rally support for causes and initiatives that resonate with their mission and values.

Beyond just financial growth, NFTs offer a protective shield to businesses against potential financial losses triggered by fraudulent activities such as counterfeit coupons.

By tokenizing your coupons, you ensure their uniqueness and traceability on the blockchain, reducing chances of forgery.

Remember, the NFT landscape is a playground that rewards innovation and creativity. So, feel free to push boundaries, experiment with ideas and let your creativity lead the way.

Utilize the steps provided on how to create an NFT, and start creating and trading your unique, potentially profitable digital assets today!

ALSO READ:

Image: Depositphotos

This article, “How to Make an NFT: A Simple Step by Step Guide” was first published on Small Business Trends